Another catalyst for China’s stock market: a higher profile in global indexes

Following 2018’s sharply negative performance for emerging-market stocks, early 2019 brought a welcome turnaround, with the MSCI Emerging Markets (EM) Index generating a 9.1% return through February.1

China’s stock market was a key driver of this strong result, as it outperformed emerging markets as a whole. Key catalysts included moves by the People’s Bank of China to reduce financial reserve requirements for commercial banks and reduce risks posed by China’s shadow banking system. In addition, the Chinese government recently implemented income-tax reforms that are expected to meaningfully increase consumer spending power.

China’s raised profile in global markets

Another potential tailwind for China’s stock market emerged on February 28—not from within China, but from outside, as part of a multi-year process that’s expanding the influence of Chinese equities on global markets. MSCI Inc. announced plans to increase the representation of Chinese domestic shares in its widely tracked global indexes by a factor of four.2

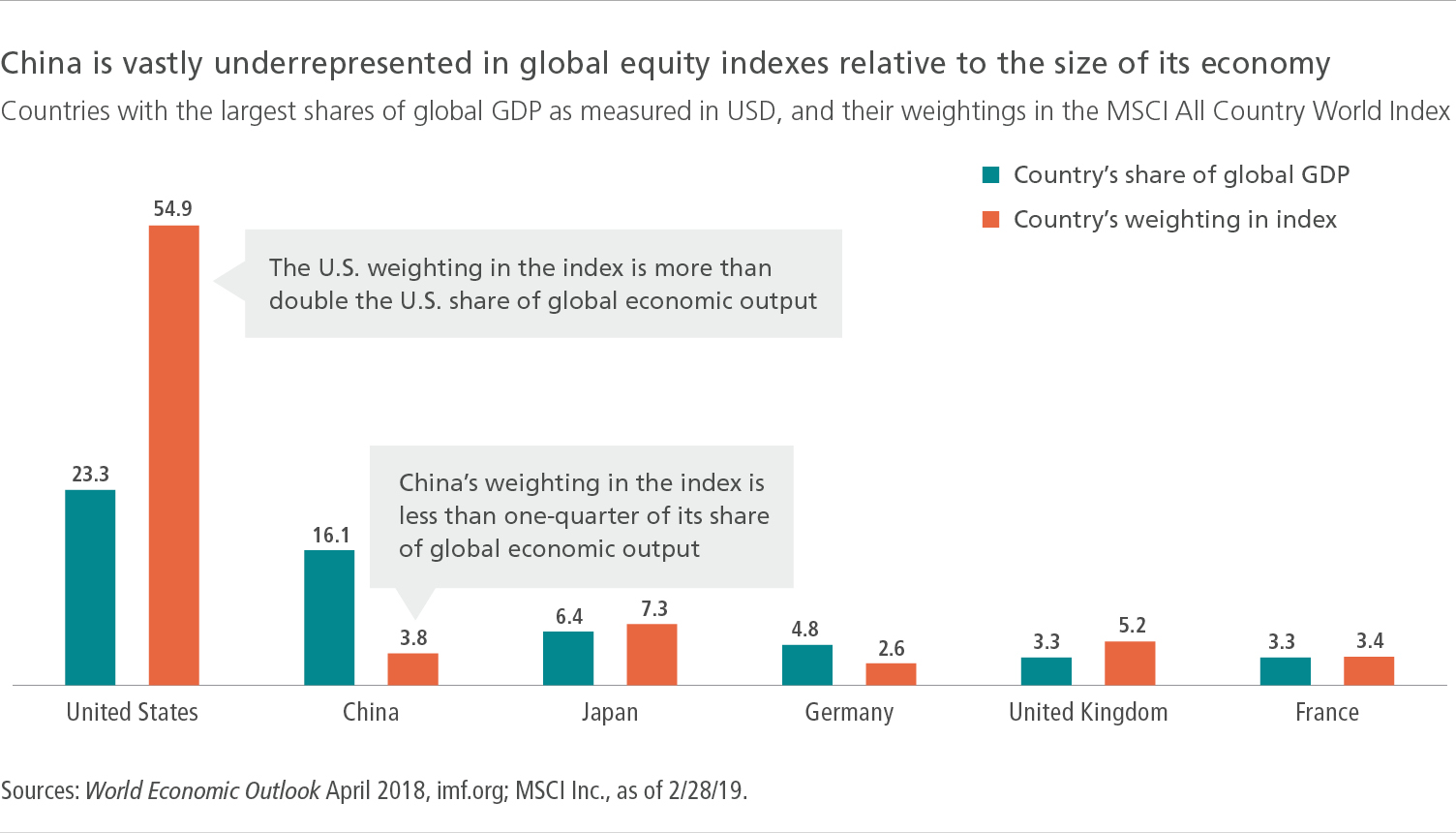

This news came nearly two years after MSCI accelerated China’s integration into global markets by taking initial steps to assign small weightings to Chinese domestic shares—known as A-shares—in benchmarks such as the MSCI EM Index and the MSCI All Country World Index (ACWI). The process began after MSCI concluded that China had sufficiently opened its markets to justify shrinking a historic imbalance that has resulted in Chinese equities being vastly underrepresented in global markets—and, consequently, in investors’ equity portfolios—relative to the size of China’s economy. China has the world’s second-largest economy, representing nearly 16% of estimated global GDP in 20183 and accounting for one-third of global growth.4 However, China’s current weighting in the MSCI ACWI is less than 4%.5

MSCI’s latest move to quadruple the weighting of China’s domestic shares in its global indexes will occur in three steps, with an inclusion factor—a mechanism used to make phased adjustments in index weightings—rising from 5% to 20% between May and the end of this year. Any future steps to increase above 20% would require Chinese authorities to address remaining questions about foreign access to its domestic equity market.

Why China’s enhanced global equity profile matters to investors—and to markets

Mutual funds and other assets that are indexed to the MSCI EM Index total about $1.8 trillion,6 and these investors will begin to increase allocations to A-shares to reflect China’s growing representation in that index as well as the MSCI ACWI. Today, China is the largest country component in the MSCI EM Index, with a 32.1% weighting—a figure that includes shares of Chinese stocks that are listed outside the domestic A-share market and accessible, within certain restrictions, to foreign investors. MSCI expects this year’s three-step process will increase its emerging-market index’s overall China weighting by 3.3%, reflecting the added representation from A-shares and other Chinese domestic shares covered by the changes.2

Taken together with other adjustments to MSCI’s weightings for emerging-market countries, as China’s weighting in the index rises, other constituent countries and territories—most notably South Korea and Taiwan—will fall in size. In our view, a full opening of the A-share market to foreign investors could eventually result in China’s weighting in the MSCI EM Index increasing significantly. Over a few years, this expansion could lead to potentially hundreds of billions of dollars flowing into Chinese companies with stocks listed on exchanges in Shanghai and Shenzhen, and many non-Chinese investors’ allocations to Chinese equities are likely to increase.

Guarded optimism for the Chinese equity market outlook

This additional share-buying activity—and the resulting expansion of foreign capital into China’s economy more broadly—may provide a modest tailwind for Chinese equities, in our view. While we expect episodes of volatility in coming months as China’s economic growth moderates and the U.S.-China trade dispute continues to play out, recent positive developments on the policy front have left us guardedly optimistic about Chinese equities broadly, and we consider it to be an under-owned market. Of particular interest to us are companies that appear poised to benefit from China’s growing middle class, its shift toward a new consumer-driven economy, and its industrial restructuring.

These trends are creating a proliferation of bottom-up investment opportunities in Chinese stocks, and the opening of the A-shares market to foreign investors is eliminating barriers that had restricted access to many of these opportunities. The growing profile of China’s domestic stocks within the global equity market is in part a recognition of the immense potential of the world’s second-largest economy.

1 FactSet, as of 2/28/19. 2 “MSCI will increase the weight of China A shares in MSCI Indexes,” MSCI Inc., 2/28/19. 3 World Economic Outlook Database, International Monetary Fund, as of 3/14/19. 4 IMF Country Report No. 18/240, People’s Republic of China, International Monetary Fund, July 2018. 5 MSCI Inc., as of 2/28/19. 6 MSCI Inc., 2019.

Important disclosures

Important disclosures

Foreign investing, especially in emerging markets, has additional risks, such as currency and market volatility and political and social instability. Investments in the Greater China region are subject to special risks, such as less developed or less efficient trading markets, restrictions on monetary repatriation, and possible seizure, nationalization, or expropriation of assets.

This commentary is provided for informational purposes only and is not an endorsement of any security, mutual fund, sector, or index.

MF787064