June 16, 2025

Model portfolios: a changing landscape that benefits advisors

Model portfolios have evolved into sophisticated solutions that offer additional benefits to financial professionals and their clients.

Please enter the email address you used when registering.

If you have a valid account with us, you will receive an email with instructions to reset your password.

An error occurred while processing your request. Please try again later.

In order to change your password, we need to verify your identity. We will send an authorization code to the email address on file.

Please enter the 6-digit code sent to your email. If you have not received a code, you may not have a registered account.

An error occurred while processing your request. Please try again later.

Enter your password to login.

In order to change your password, we need to verify your identity. We will send an authorization code to the email address on file.

Enter the 6-digit code sent to your email

An error occurred while processing your request. Please try again later.

In order to change your phone number, we need to verify your identity. We will send an authorization code to the email address on file.

Enter your password to login.

To verify your identity, we need to send an authorization code to the email address on file.

Enter the 6-digit code sent to your email

An error occurred while processing your request. Please try again later.

We need a phone number to keep your account secure. We will send you a code to validate your phone number.

Please enter the email address you used when registering.

If you have a valid account with us, you will receive an email with instructions to reset your password.

An error occurred while processing your request. Please try again later.

In order to change your password, we need to verify your identity. We will send an authorization code to the email address on file.

Please enter the 6-digit code sent to your email. If you have not received a code, you may not have a registered account.

An error occurred while processing your request. Please try again later.

Enter your password to login.

In order to change your password, we need to verify your identity. We will send an authorization code to the email address on file.

Enter the 6-digit code sent to your email

An error occurred while processing your request. Please try again later.

In order to change your phone number, we need to verify your identity. We will send an authorization code to the email address on file.

We have sent an email to {0}. Click the link in the email to finish setting up your dashboard

Please enter the email address you used when registering.

If you have a valid account with us, you will receive an email with instructions to reset your password.

An error occurred while processing your request. Please try again later.

In order to change your password, we need to verify your identity. We will send an authorization code to the email address on file.

Please enter the 6-digit code sent to your email. If you have not received a code, you may not have a registered account.

An error occurred while processing your request. Please try again later.

Enter your password to login.

In order to change your password, we need to verify your identity. We will send an authorization code to the email address on file.

Enter the 6-digit code sent to your email

An error occurred while processing your request. Please try again later.

In order to change your phone number, we need to verify your identity. We will send an authorization code to the email address on file.

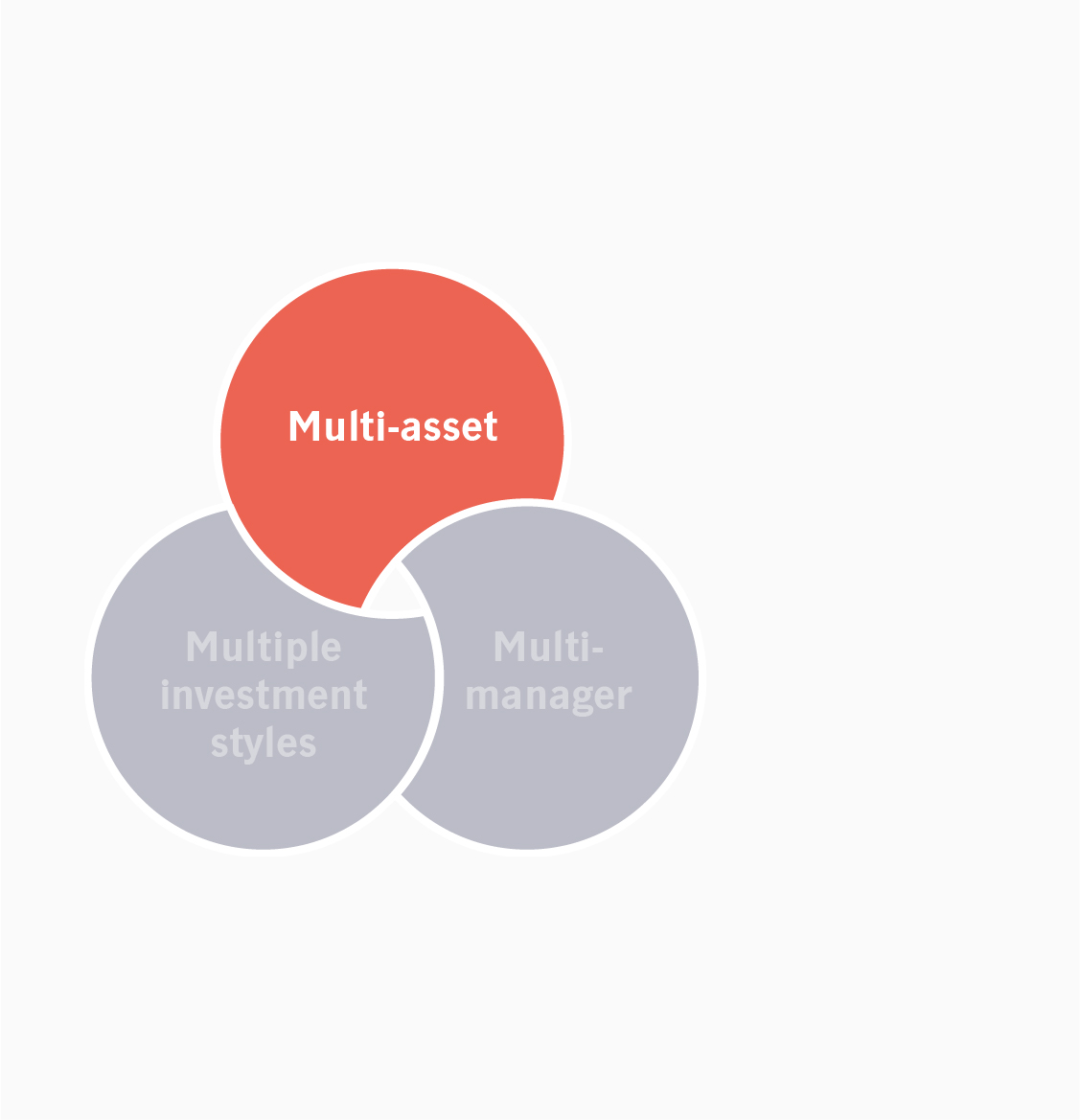

We believe a multi-asset investment approach is best suited to provide an appropriate level of diversification and risk-adjusted return potential that can help retirement savers pursue their long-term goals.

Now's the time to consider how much additional value your target-date funds offer. With Manulife John Hancock Investments, participants can gain access to multiple offerings, the benefits of one-stop shop, results for retirement, and expenses that can fit any plan's budget.

We offer flexible retirement saving options to give participants greater choice. Our Lifetime glide path addresses longevity risk that many participants face during retirement, and can be chosen within a mutual fund or collective investment trust vehicle.

We offer a range of funds managed by in-house and third-party managers giving investors ample choice through one investment platform.

We believe target-date funds should take a more granular approach to accessing opportunities across the asset class spectrum. In our view, investors can no longer rely on traditional equity and government bonds as the only key sources of diversification and return potential. With our risk-aware focus, coupled with our depth of expertise in multi-asset strategies, we seek to give investors comprehensive options for pursuing the capital growth necessary to generate income in retirement.

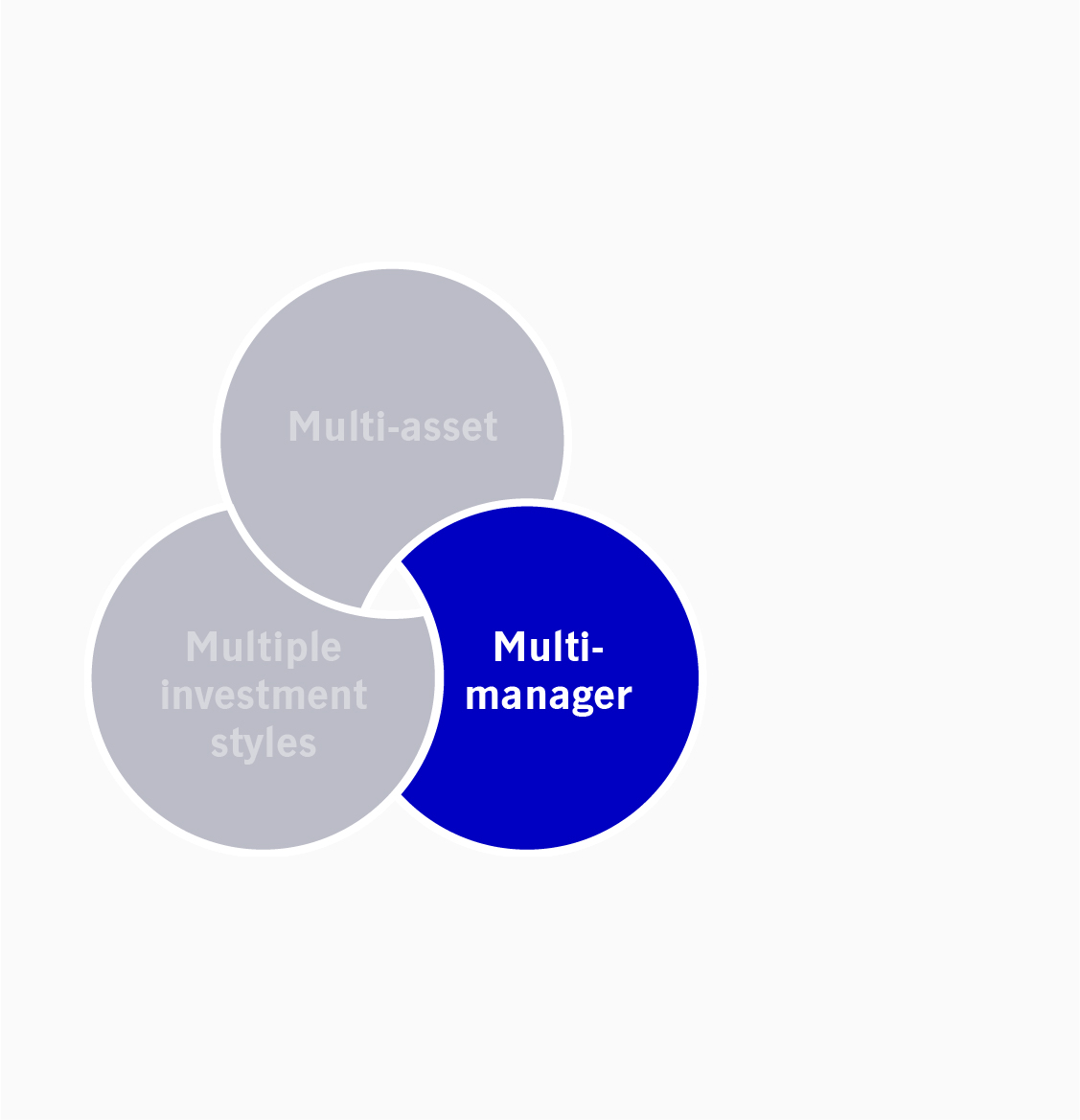

We believe no one manager can be the best at everything. Our deliberate open-architecture1 approach allows us to combine a deep history of managing multi-asset and income solutions for participants, with finding some of the best managers across select asset classes and investment styles. The results are robust target-date fund options suited to today’s investing environment.

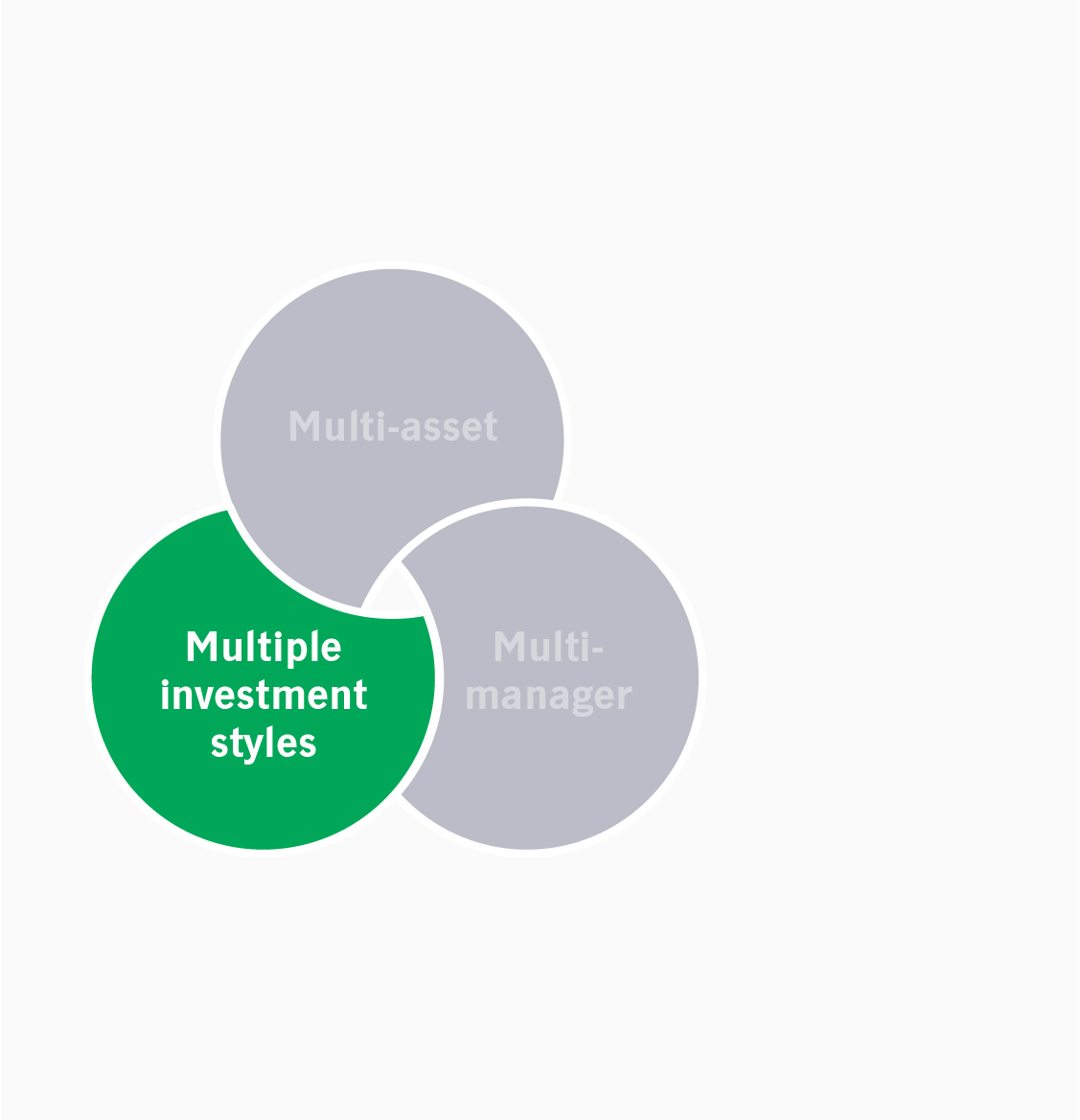

We believe investors should have access to both passive and active investment approaches. Within certain asset classes, there can be benefits to using one style over another depending on your individual situation. Our target-date approaches have the flexibility to combine lower-cost, passive strategies that have the opportunity to provide market exposure together with actively managed strategies where we believe they can be most effective.

Source: John Hancock Investment Management, as of 3/31/25. For illustrative purposes only.

Plan participants face numerous challenges in the search for higher-returning, lower-risk investment options. That's why our range of target-date funds helps empower fiduciaries in choosing an optimal option for their participants.

Our Lifetime Blend Portfolios are one-stop retirement investments, with a focus on low-cost implementation.

Our Multimanager Lifetime Portfolios are one-stop retirement investments, emphasizing allocations to active asset class specialists.

Despite expenses coming down in recent years, the average net expense ratio for target-date funds is 64 basis points.¹ Our expenses are below average for both our actively and passively implemented target-date funds.

Total expense ratios are below average for both actively and passively implemented John Hancock target-date funds.

1 Morningstar, 2025. Average total expense of all open-end target-date funds that are tracked by Morningstar. For Class R6 shares, as of 3/31/25.

Periods of market downturns are stressful for all investors; however, historical data shows that participants are often rewarded through higher long-term returns. Encouragingly, even participants retiring as markets enter a downturn have an opportunity to recoup losses.

To those just entering retirement, news of inflation, market volatility, rising interest rates, and the possibility of recession can be especially alarming. Here are tips to help feel better prepared.

SECURE Act 2.0 of 2022 was signed into law on December 29, with policy changes that will affect both the administrators of and participants in qualified retirement plans and IRAs. We’ve put together a guide to help you navigate the provisions that may matter most to you.

For the sixth year in a row, that’s more allies than any other firm on the list from the National Association of Plan Advisors

For complete information and criteria, visit napa-net.org/napa-advisor-allies-2024

June 16, 2025

June 11, 2025

June 4, 2025

Retirement plan advisors and sponsors: Ask a Manulife John Hancock Investments Retirement Investment Consulting (RIC) specialist for a detailed review of how John Hancock Lifetime Blend Target-Date Portfolios can fit into your plan or practice.

Request a meeting with a Manulife John Hancock Investments business consultant

* indicates a required field

Thank you

Your submission was successful

Diversification does not guarantee a profit or eliminate the risk of a loss.

The target date is the expected year in which investors in a target-date portfolio plan to retire and no longer make contributions. The investment strategy of these portfolios is designed to become more conservative over time as the target date approaches (or, if applicable, passes) the target retirement date. Investors should examine the asset allocation of the portfolio to ensure it is consistent with their own risk tolerance. The principal value of your investment, as well as your potential rate of return, is not guaranteed at any time, including at, or after, the target retirement date.

The glide path is the asset allocation within a target-date strategy that adjusts over time as participants' age increases and their time horizon to retirement shortens. The basis of the glide path is to reduce the portfolio's chance of loss as the participants' time horizon decreases. The asset mix of each portfolio is based on a target date, which is the expected year in which participants in a portfolio plan to retire and no longer make contributions. A team of asset allocation professionals adjusts each portfolio's investments over time to ensure a noticeable and steady shift from equities to fixed income in the years leading to retirement or during retirement, if applicable. Investors should examine the asset allocation of the portfolio to ensure it is consistent with their own risk tolerance. In developing the glide path, it was assumed that participants would make ongoing contributions during the years leading up to retirement and stop making those contributions when the target date is reached. The principal value of your investment, as well as your potential rate of return, is not guaranteed at any time, including at, or after, the target retirement date.

Portfolio performance depends on the advisor’s skill in determining asset class allocations, the mix of underlying funds, and the performance of those underlying funds. The underlying funds’ performance may be lower than the performance of the asset class that they were selected to represent. The portfolio is subject to the same risks as the underlying funds and ETFs in which it invests: Stocks and bonds can decline due to adverse issuer, market, regulatory, or economic developments; foreign investing, especially in emerging markets, has additional risks, such as currency and market volatility and political and social instability; the securities of small companies are subject to higher volatility than those of larger, more established companies; and high-yield bonds are subject to additional risks, such as increased risk of default. Owning an ETF generally reflects the risks of owning the underlying securities it is designed to track, which may cause lack of liquidity, more volatility, and increased management fees. Hedging and other strategic transactions may increase volatility of a portfolio and could result in a significant loss. Each portfolio's name refers to the approximate retirement year of the investors for whom the portfolio's asset allocation strategy is designed. The portfolios with dates further off initially allocate more aggressively to stock funds. As a portfolio approaches or passes its target date, the allocation will gradually migrate to more conservative, fixed-income funds. The principal value of each portfolio is not guaranteed and you could lose money at any time, including at, or after, the target date. Liquidity—the extent to which a security may be sold or a derivative position closed without negatively affecting its market value, if at all—may be impaired by reduced trading volume, heightened volatility, rising interest rates, and other market conditions. Please see the portfolios' prospectuses for additional risks.

© 2025 Morningstar, Inc. All rights reserved. The information contained herein (1) is proprietary to Morningstar and/or its content providers, (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance does not guarantee future results.

John Hancock Retirement Plan Services LLC offers administrative and/or recordkeeping services to sponsors and administrators of retirement plans. John Hancock Trust Company LLC, a New Hampshire non-depository trust company, provides trust and custodial services to such plans, offers an Individual Retirement Accounts product, and maintains specific Collective Investment Trusts. Group annuity contracts and recordkeeping agreements are issued by John Hancock Life Insurance Company (U.S.A.), Boston, MA (not licensed in NY), and John Hancock Life Insurance Company of New York, Valhalla, NY. Product features and availability may differ by state. Securities are offered through John Hancock Distributors LLC, member FINRA, SIPC.

John Hancock Investment Management Distributors LLC is the principal underwriter and wholesale distribution broker-dealer for the John Hancock mutual funds, member FINRA, SIPC.

NOT FDIC INSURED. MAY LOSE VALUE. NOT BANK GUARANTEED.

MF4511286